Adverse selection is a classic problem in health insurance. If you offer insurance to individuals, you may want to set the premiums based on the average price of the population you plan to cover. At this price, however, the sickest patients are the ones most likely to take up insurance and the health insurer’s expenses are likely to be higher than expected. This may result in an adverse selection death spiral. One alternative is to mandate that all individuals purchase health insurance, but government mandates are often unpopular and the level of coverage that is mandated also would have to be determined.

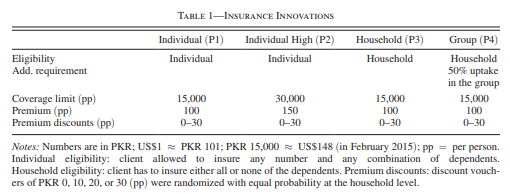

A paper by Fischer, Frölich, and Landmann (2023) aims to quantify the degree of adverse selection in hospital insurance plans for individuals in Pakistan. Pakistan has about 250 million individuals and annual per capita GDP is $5,200 (CIA World Factbook). To measure the amount of adverse selection, the authors collaborated with the National Rural Support Programme of Pakistan (NRSP) to offer different types of insurance to individuals across 83 different villages. Each village could be offered individual insurance (P1) with a 15,000 PKR out-of-pocket maximum or a more generous individual insurance (P2) with a 30,000 PDR out-of-pocket maximum. Other villages were assigned to household insurance (P3) where all individuals in the household are required to enroll in the insurance and a “Group policy” where >50% of a credit group or community organizations (COs) are required to enroll in the insurance. The table below summarizes these options.

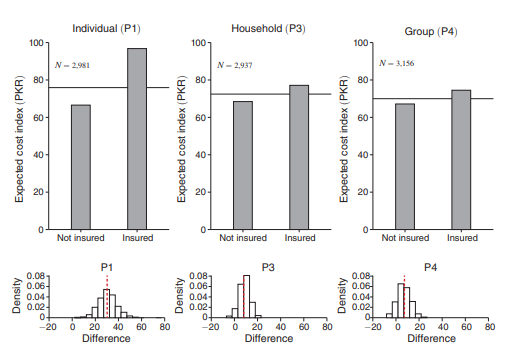

Using this approach, the authors find that there was:

…substantial selection in individual policies, leading to welfare losses and the threat of a market breakdown. Bundling insurance policies at the household level or higher almost eliminates adverse selection, thus mitigating its welfare consequences and facilitating sustainable insurance supply

One can clearly see this result from the figure below. One important point to note is that average household size in the experiment was 5.99. Thus, it is unclear if adverse selection would be mitigated to the same degree in higher-income countries where household size is smaller.

The full article is available here.