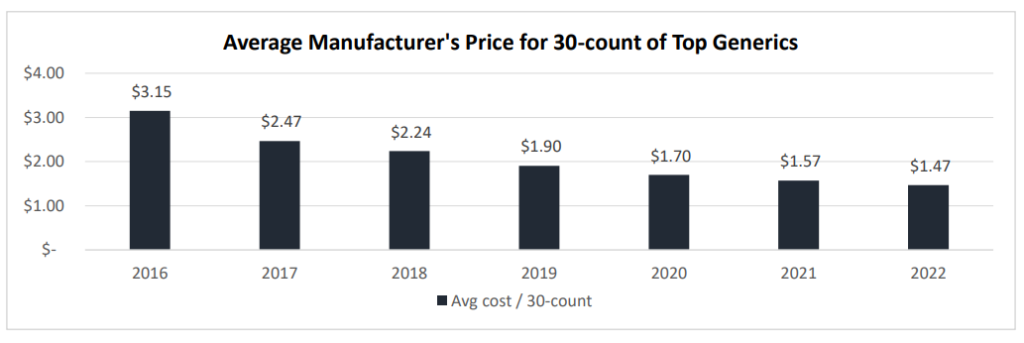

One piece of good news for consumers is that generic prices are falling. However, generic prices may be falling so much that drug shortages are occurring (which is not a good thing). Data from a working paper by Sardella (2023) finds a dramatic drop in generic prices in recent years.

The authors claim that shortages in generic drugs are caused by three primary reasons: (i) low profitability, (ii) low value for quality, and (iii) complex, global supply chains.

With no distinguishing product differentiation or quality tracking [e.g., reputation] in the industry to distinguish product quality differences, market competition in the generic drug industry, without market exclusivity, focuses on the dimension of price.

Price competition is especially intense because 3 large pharmacy benefit managers (PBMs) control 92% of the US market. Price competition has lead most generic drugs are manufactured outside the US. According to the FDA:

…as of August 2019, 72% of FDA-approved API manufacturing facilities were outside of the US. A recent 2021 deeper dive revealed that approximately 75% of COVID-19 related drugs, 97% of antibiotics, 92% of antivirals, and 83% of the top 100 generic drugs consumed have no US-based source of APIs

Foreign markets are attractive because of government subsidies, lower costs of labor, and less regulatory oversight. However, because quality is not reimbursed, there are some issues:

- Greater than 80% of APIs for FDA-defined essential medicines and over 90% of top antibiotics and antivirals have no US manufacturing source

- Less than 5% of large-scale API sites, globally, are located in the US – the majority of large-scale manufacturing sites are in India and China

- India and China have the greatest number of API facilities supplying the US market and over ten percent of these facilities have an FDA Warning Letter1

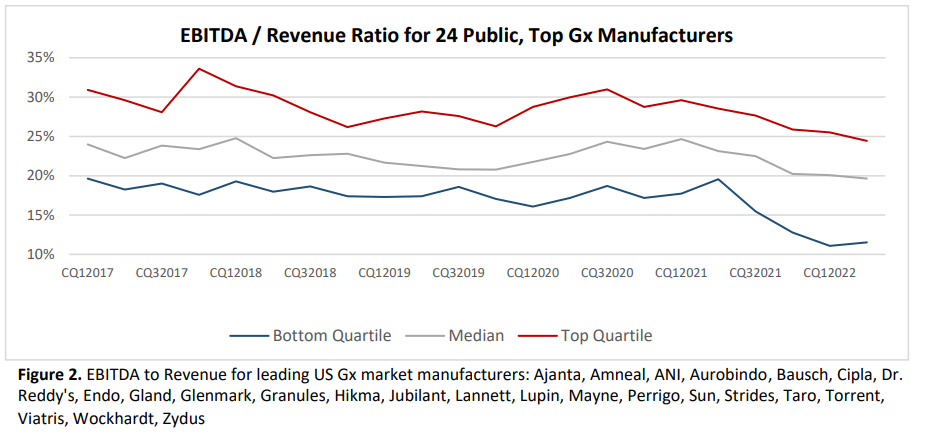

Overall, being a generic drug manufacturer is not a great business. EBITDA (Earnings before interest, taxes, depreciation and amortization) has fallen in recent years. Return on investment has fallen from close to 10% in 2013 to just 5% in 2023.

Because margins are so low, there is little room to invest in quality. Moreover, compliance with FDA quality standards is falling.

…the rate of industry close-out of regulatory issues (i.e., issues resolved to the FDA’s standards) has dropped from one-in-four warning letters closed out to one-in-twenty by 2022… 26% of the nation’s prescriptions now being supplied by companies that have received warning letters since 2020.

The author proposes 3 solutions to the problem which you can read here.